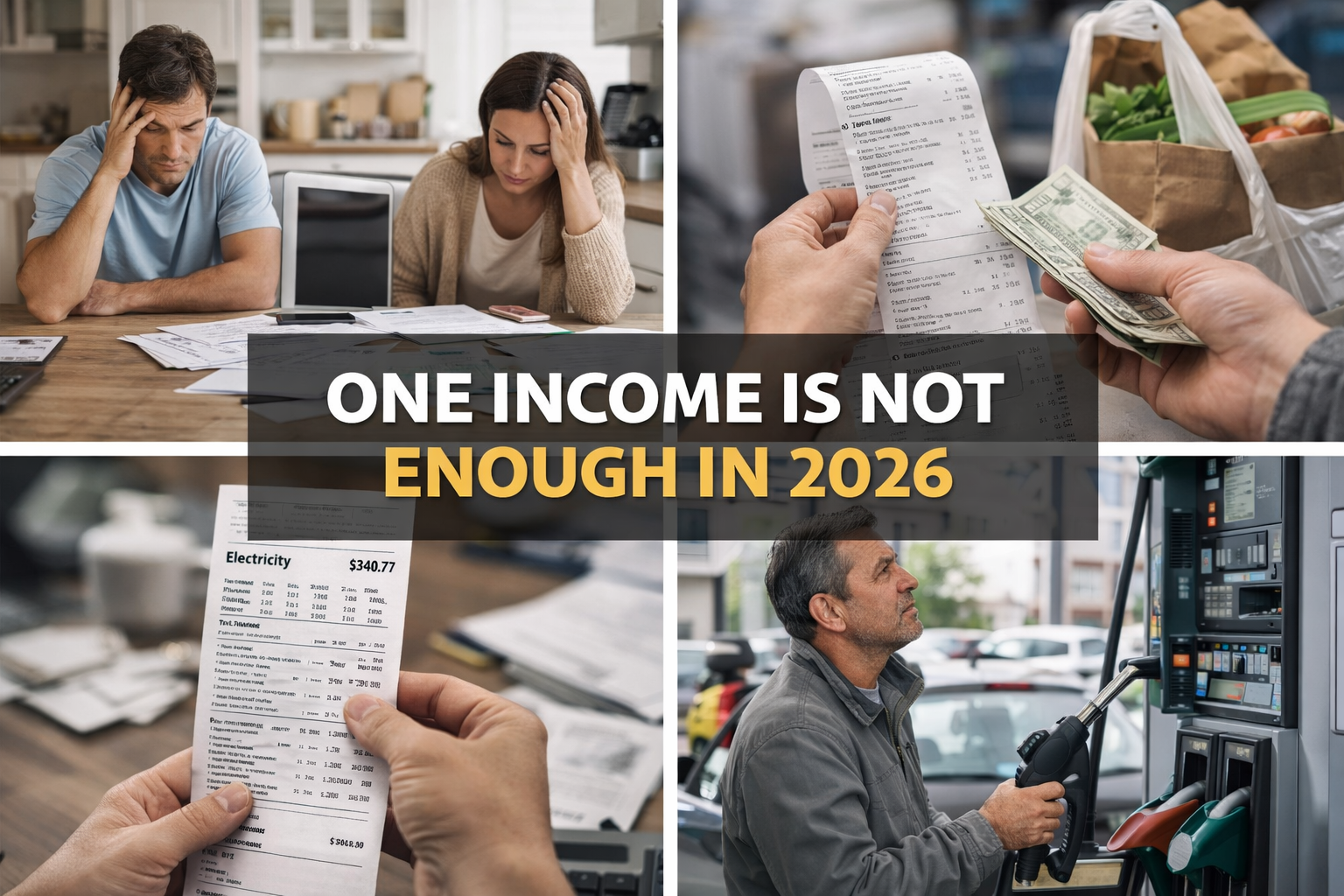

One income is not enough in 2026—and many households are already feeling the shift.

Global instability is no longer a distant headline—it is quietly reshaping everyday life.

From rising fuel prices to unstable currencies and unpredictable job markets, the effects of geopolitical and economic shifts are now being felt directly at the household level.

Recent global data shows that while inflation has come down from its peak, it is still hovering around 3.7%–3.8% globally in 2026, which remains above long-term stability targets.

At the same time, economic growth is slowing, and uncertainty is rising due to ongoing geopolitical tensions.

This creates a difficult reality:

Costs remain high, but income growth is slowing.

And for many households, one conclusion is becoming unavoidable:

One income is not enough to maintain financial stability anymore.

1. What’s Actually Changing in 2026

Geopolitical crises may seem distant, but their economic effects follow a very real chain reaction. This is where many people realize that one income is not enough to handle rising living costs. The jobs that are safe in the recession

Here’s how it actually plays out:

- Energy disruptions are directly increasing fuel and transportation costs, especially as conflicts affect oil and gas supply routes. UN Food and Agriculture Organisation projections indicate that global prices could average 15% to 20% higher in the first half of 2026 if the crisis persists.

- Global trade instability is slowing down supply chains, which leads to shortages or delayed availability of essential goods—often pushing prices higher even when demand hasn’t increased.

- Currency fluctuations are reducing purchasing power, meaning even if your salary stays the same, your real spending ability declines over time.

- Economic uncertainty is forcing companies to slow hiring or freeze expansion, reducing job mobility and income growth opportunities.

What’s different now is not just the impact but the speed at which global events affect local life.

A disruption anywhere now reflects in your expenses within weeks, not years.

2. How This Is Affecting Everyday Life

1. Rising Cost of Living

- Everyday essentials like food, fuel, and utilities are increasing steadily—even in regions where overall inflation appears “stable” on paper.

- Housing costs continue to rise due to demand pressure and financing costs, making rent and home ownership more difficult.

- Even when inflation slows statistically, prices rarely go back down—they stabilize at higher levels, locking in long-term cost increases.

2. Income Pressure

- Wage growth is not keeping up with real living costs, creating a silent gap between income and expenses.

- Global growth projections for 2026 are modest (around 3.3%), meaning fewer opportunities for rapid income expansion.

- Freelancers and contract workers are facing demand fluctuations due to business uncertainty and reduced spending.

3. Psychological Shift

- Financial stress is becoming more common—even among middle-income households.

- Long-term planning (saving, investing, upgrading lifestyle) is being replaced with short-term financial adjustments.

- People are shifting from “How do I grow?” → to “How do I sustain?”

The result is clear: People are no longer trying to build wealth—they are trying to protect stability.

3. Why One Income Is Not Enough in 2026

For decades, financial planning was based on a simple assumption:

| One stable job can support a household | But today 2026 |

| That assumption depended on: • Predictable inflation • Stable employment • Gradual economic growth | • Inflation remains structurally higher than historical comfort levels • Global shocks are more frequent and interconnected • Job stability is decreasing due to automation and economic shifts |

This is not about working harder. It’s about reducing dependency risk.

Think of it like system design: 1. One income = single point of failure 2. Multiple incomes = built-in redundancy and resilience

4. The Shift Toward Digital and Flexible Income

This is why more people are moving toward digital and flexible income models.

Not because they are easy but because they solve structural problems.

Digital income offers:

- Access to global markets, reducing reliance on local economic conditions

- Scalability, meaning effort today can generate income later

- Flexibility, allowing income diversification without leaving a primary job

- Lower entry barriers, compared to traditional business models

In uncertain environments, flexibility becomes a form of security. This is why the mindset is changing:

From “extra income” → to “essential income”

5. Practical Ways to Build Additional Income

The biggest mistake people make here is overcomplicating things.

The goal is not to do everything, it’s to do one thing well.

| Skill-Based Income: 1. Freelancing /consulting allows you to convert existing skills into income relatively 2. Works best for technical, creative, or analytical skill sets ✔ Faster monetization ✖ Limited by time |

| Digital products: 1. Templates, SVGs, guides, or niche content can generate recurring income 2. Requires upfront effort but scales over time ✔ Scalable ✖ Slow start |

| Remote & Contract Work: 1. Adds a second income stream with relatively predictable earnings 2. Increasingly common in global job markets ✔ Stable supplement ✖ Time-dependent |

| Content-Based Income: 1. Blogging, YouTube, or niche content platforms 2. Builds long-term income assets ✔ Compounding growth ✖ Requires consistency |

6. Where Most People Go Wrong

The issue isn’t lack of opportunity, it’s poor execution.

| Common Mistakes | A More Effective Approach |

| • Trying multiple income streams at once without focus • Following trends instead of building skills • Expecting quick income instead of gradual growth This leads to burnout, not financial stability. | • Start with one additional income stream • Choose something aligned with your strengths • Build consistently over time Adapting to this new reality doesn’t require drastic changes just a better structure. |

7. Practical Steps to Overcome the One-Income Problem (2026)

1. Build a Financial Buffer First

Start with a safety net of 3–6 months of essential expenses. Without this, even a small disruption can turn into a financial crisis. Consistency matters more than amount—small, regular savings work.

2. Strengthen Your Primary Income

Before chasing new income streams, stabilize your main one. Focus on skills and roles that are harder to replace and tied to real-world demand. A weak primary income cannot be fixed by side hustles.

3. Add One Reliable Secondary Income

Avoid the trap of juggling multiple side hustles. Start with one controlled and realistic stream—digital products, freelance work, or small-scale production. Simplicity increases your chances of success.

4. Prioritize Scalable Income Sources

Shift toward income that does not depend entirely on your time. Digital products, repeatable services, or small production models allow growth without constant effort.

5. Reduce Unnecessary Expenses

Increasing income alone is not enough. Identify and cut recurring financial leaks like unused subscriptions, high-interest debt, or lifestyle inflation.

6. Build Future-Proof Skills

Focus on skills that work globally and remain relevant—technical expertise, digital marketing, and practical use of AI tools. These multiply earning potential over time.

7. Create Systems, Not Hustles

Long-term stability comes from systems that run with minimal involvement. Combining platforms like e-commerce, content, and social traffic can create consistent income flows.

8. Plan for Uncertainty

Economic instability is no longer an exception. Build your finances assuming disruptions will happen, not hoping they won’t.

8. Conclusion

The reality that one income is not enough is no longer theoretical—it is practical. Economic instability is not temporary—it is reshaping how financial systems function.In fact, as economic uncertainty grows, many people are already shifting toward more stable career paths—something we explored in detail in our guide on jobs safe in a recession in 2026.

| The old model | The new reality |

| One job One income Predictable future | Multiple income streams Flexible earning models Resilience over dependence |

Recognizing that one income is not enough is not negative; it is an adaptation. And those who adapt early won’t just survive, they will operate with far greater control in an uncertain world.

FAQ

1. Why is one income not enough anymore?

Because living costs remain elevated while income growth is slower, creating a gap that a single income often cannot cover.

2. Is inflation still a problem in 2026?

Yes. Even though global inflation has decreased from peak levels, it is still around 3.7–3.8%, which keeps overall costs high.

3. Why are living costs still high if inflation is falling?

Because inflation measures the rate of increase, not price levels. Prices stabilize at higher levels rather than decreasing.

4. What is the safest way to build a second income?

Start with one skill-based or digital income stream that aligns with your existing capabilities.

{kind=link}